In the food retail sector smaller and independent businesses are struggling to remain profitable due to fierce competition and high price pressure.

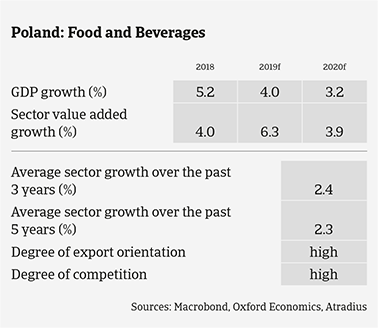

Food is one of Poland’s strongest industries, accounting for a 9% share in the EU food industry. Domestic and export demand continue to grow, with almost 4% value added growth expected in 2020..

Competition in the Polish food market is high, especially on price. While profit margins for most businesses are stable, they generally remain at a low level. Higher profits are only generated by larger entities or small specialised players, while many smaller and mid-sized businesses struggle to perform well. The ongoing consolidation process is rather slow, as many small and family-owned companies are reluctant to sell their business, with the decision to do so often coming too late (e.g. when a business is already facing severe liqudity problems).

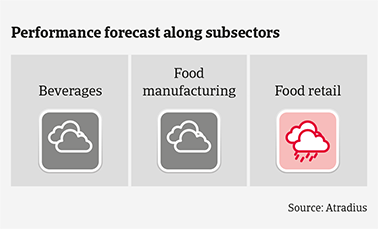

The dairy segment is mainly controlled by four large companies and shows stable growth rates (value added is expected to increase 5.6% in 2019 and 3.9% in 2020). The level of overdue and non-payments is low.

Within the meat segment the white meat subsector is performing well. Poultry farming has shown robust growth rates for several years, and Poland has become one of the largest poultry meat producers in the EU. However, the red meat segment struggles with low margins, price pressure, a slow consolidation process and the repercussions of repeated outbreaks of African swine fever on Polish commercial farms. The level of non-payments and insolvencies is high and increasing in this segment.

The food retail sector is characterised by fierce competition, high price pressure and changing consumer behaviour (price-sensitiveness). Smaller and independent retailers are mainly affected, with many struggling to remain profitable, working on tiny and even negative margins. The number of payment delays and insolvencies remains elevated.

Financing requirements and financial gearing are high in the food industry, and low interest rates still support further investments. The average payment duration in the Polish food industry is 30 days. The number of protracted payments is generally high, as larger businesses use their leverage against suppliers demanding long payment terms or to prolong payments in order to improve their own cash flow.

Insolvencies are expected to increase by 3% annually in 2019 and 2020. Food retailers and businesses active in the red meat segment are mainly affected.

Due to the differences in business performance and credit risk our underwriting varies by subsector. We are open for Polish dairy businesses, as this segment is currently doing well, and neutral for beverages, where price competition is an issue. We are restrictive for the red meat segment and food retail due to the issues mentioned above.

Fraudulent events are a concern in both domestic and export business transactions throughout all food subsectors, but most prominent in the fruit and vegetables and meat segments. While the awareness within companies has increased, the number of fraud attempts is still rising.

Related documents

1.19MB PDF